2nd Omnibus Law/General Rules for National Tax Law (KUP)

Continuing from last month, I would like to talk about sanctions (penalties) under the Omnibus Act and the Act on General Rules for National Taxes. Many people may have the impression that Indonesian taxes have a high penalty of 2% per month on everything. Basically, there is an upper limit of 24 months (48%), but since tax audits are conducted over a year, in many cases where additional tax is imposed, a penalty of 30% or more is incurred, placing a heavy burden on taxpayers. How have penalties changed as a result of the Omnibus Law, which aims to facilitate business operations?

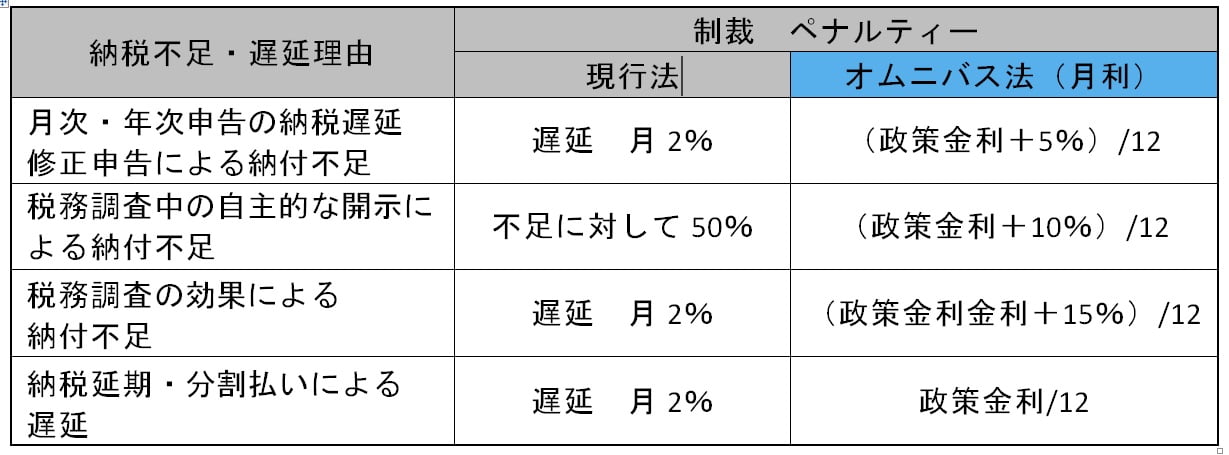

Main sanctions

The interest rate of the penalty imposed is now different depending on the reason for the delay. Do I check the policy interest rate and do the above calculation every month? You may think that the calculations are troublesome. In actual practice, at the end of each month, the results of the monthly interest calculation for the following month are announced as an ordinance by the Minister of Finance, so there is no need to calculate them yourself using the above formula. The monthly policy interest rate for February 2021 announced at the end of January 2021 is 0.51%, so using the above calculation formula, the maximum interest rate is 15% plus, but the calculation result is still 1.76%, which is lower than the previous 2%. The calculation method is to select the interest rate for the month in which the sanction starts date falls from the Minister of Finance Ordinance and multiply it by the number of months in question. Any period of less than one month is counted as one month, and the maximum period of 24 months is the same as before. Sanctions for deficiencies such as late issuance, non-issuance, or incomplete FP (Faktur Pajak) VAT invoices, which are necessary for VAT (value added tax) processing, are also reduced from the previous 2% per month to 1% of the VAT taxable amount under the Omnibus Law. Regarding VAT, there are not only penalties but also amendments, so next month I would like to discuss VAT starting with the Omnibus Law.

Related laws and regulations: UU 11 Year 2020 Tentang Cipta Kerja (Omnibus method) Pasal 111